This Week in Critical Minerals - #4

Indian lithium discovery, copper in the DRC, nickel trading fraud, and another DOE loan

Welcome to the fourth issue of This Week in Critical Minerals, where I cover the mining and resource processing projects and technologies being built around the world.

Thank you for joining me. Let’s dig into it.

Lithium

Lithium discovered in Jammu and Kashmir, India

India’s Ministry of Mines announced a discovery of 5.9 million tonnes of lithium on Thursday in the Jammu and Kashmir region. This means India possesses the 7th largest lithium reserves in the world, following Bolivia, Argentina, the US, Chile, Australia, China (according to USGS). The geology of the deposit is not known, but discoveries of lepidolite and spodumene (hard-rock lithium minerals) have been made in other areas of the country — in contrast with the lithium brines found in major producers like Chile and Argentina. Though a breakthrough development for India’s electric vehicle ambitions, this deposit will likely take a decade or more to develop, meaning the discovery won’t impact manufacturing until the mid-2030s. Benchmark Mineral Intelligence CEO Simon Moores summarizes the takeaways well.

Waste rock study ordered for Thacker Pass

Last week I discussed the Thacker Pass mine proposal in Nevada, and I stated that a judge’s decision on the fate of the project was imminent. That decision is now in, but the outcome is still unclear. The Federal District Court of Nevada judge ruled that all objections to the proposed mine are invalid, but the Bureau of Land Management must determine whether Lithium Americas can dump waste rock on the site. The company is confident this review is an easy fix and plans to begin construction this summer, says CEO Jonathan Evans. Just two weeks ago GM announced a $650MM investment in Lithium Americas, and if developed, Thacker Pass will be the largest lithium mine in the US.

Copper

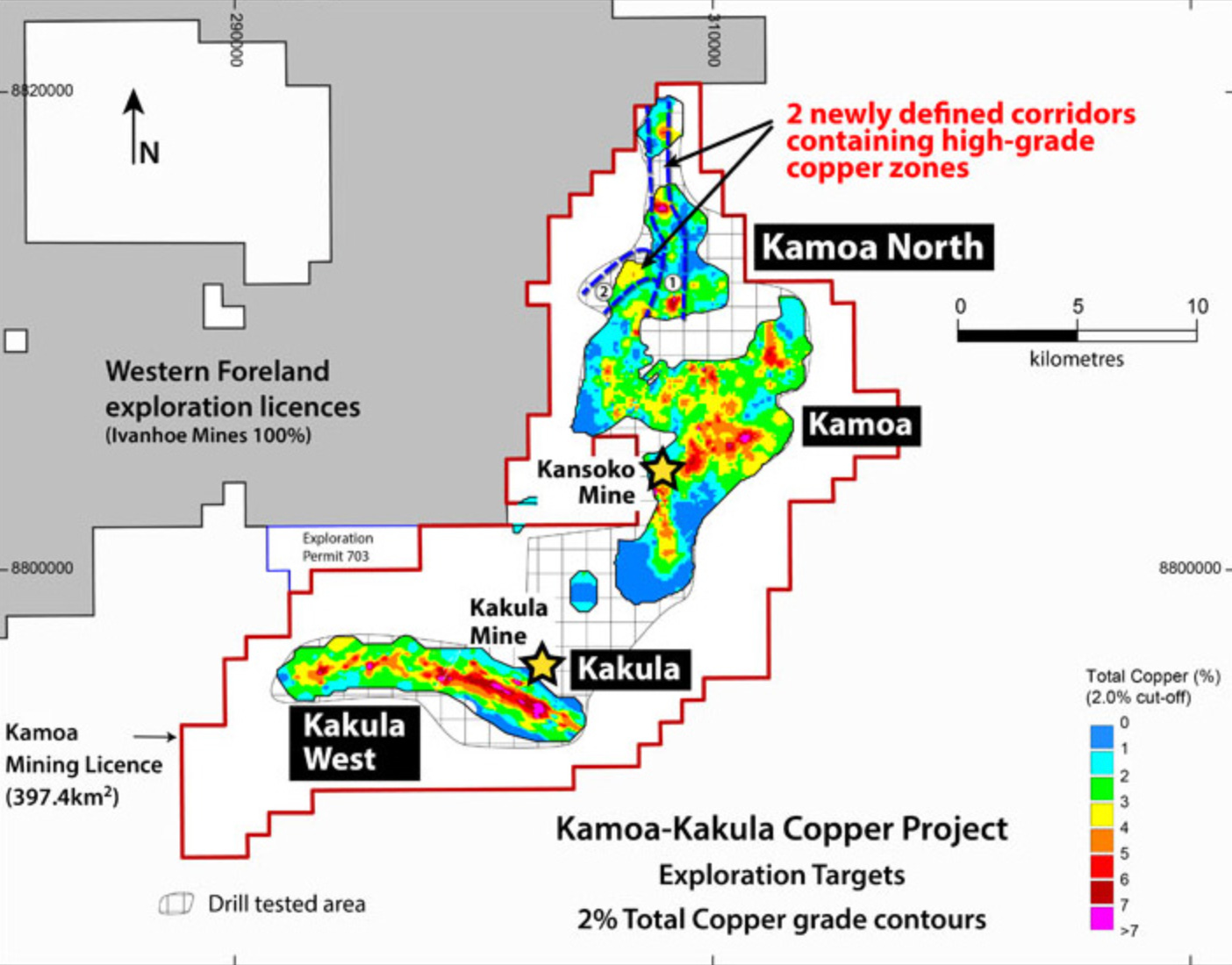

Ivanhoe Mines in talks to increase activities in Congo

Robert Friedland’s Ivanhoe Mines is seeking a strategic partner to develop copper assets in the Democratic Republic of the Congo (DRC). Ivanhoe operates their flagship Kamoa-Kakula copper mine in the DRC, of which they own 39.6%. Partner Zijin Mining owns 39.6% of the project, with Crystal River Global Limited and the Congolese government comprising the rest of the ownership (0.8% and 20%, respectively). The company has been in touch with BHP and sovereign investors about taking a minority stake in exploration of adjacent land (Western Foreland Project), as countries and companies seek to quickly ramp up copper production. The Kamoa-Kakula mine produced 333,500 tonnes of copper in 2022, quickly ramping up from 105,884 tonnes in 2021, the first year of production at the mine. The project could be one of the largest copper mines in the world very soon, producing 600,000 tonnes per annum (tpa) by the end of 2024.

ERG to double copper/cobalt output in Africa

Eurasian Resources Group, mining conglomerate with assets across Central Asia and Africa, will spend $1.8B to double their cobalt and copper production in Africa. ERG currently produces 200,000 tpa of copper and 25,000 tpa of cobalt, primarily in the DRC. A significant portion of the capital will go towards building small hydro plants as well as solar and batteries to mitigate disruptions from an erratic electric grid. The company, controlled by the Republic of Kazakhstan and a trio of Kazakh oligarchs which faced a serious fraud investigation in 2013, was restructured in 2014 with $2.5B of financing from China as part of the Belt and Road Initiative.

Further investment by ERG and Ivanhoe show that money will continue to flow into the mineral-rich DRC to develop existing copper and cobalt assets. Exploration timelines are too long to meet emerging electric vehicle demand, so expanding existing projects looks like the only serious way to meet demand in the short-term.

Nickel

GM bidding for stake in Vale base metals business

Last year Vale announced that it would split off its copper and nickel (base metals) business from its iron ore business, and then sell a portion (potentially $2B) of the new base metals company to a strategic partner. The company’s stock had been trading at a lower earnings multiple than base metals peers, so separating the businesses could unlock massive shareholder value. GM has advanced in this bidding, along with Saudi Arabia’s Public Investment Fund and Japanese trading house Mitsui & Co. Vale is already a supplier of nickel to Tesla, has signed a supply agreement with GM, and is developing a nickel processing plant in Indonesia with Ford.

GM’s potential investment in the Vale base metals business follows their recent investment in Lithium Americas, and shows that auto manufacturers are investing heavily to secure raw material for mineral-intense electric vehicles.

Trafigura loses $577MM in alleged fraud

Global commodity trader Trafigura is reported to have lost $577MM in a nickel fraud involving companies owned by Indian businessman Prateek Gupta. Trafigura had paid for shipments of nickel but received cargo of much lower value. Last July the Indian intelligence agency Central Bureau of Investigation opened an investigation against Gupta over a separate alleged fraud. Commodities trading can be an opaque business where profit is made navigating the complexities of balancing global supply chains, and sometimes this involves doing business with dubious characters. This leads to missing metals being a prevalent issue, as in last August when Glencore halted shipments to Chinese firm Huludao Ruisheng after half a billion dollars of copper went missing.

Batteries

Redwood Materials secure $2B DOE loan

Battery recycling company Redwood Materials will receive a $2B loan from the Department of Energy to develop anode and cathode materials manufacturing plants in the US. Redwood was founded by Tesla cofounder JB Straubel in 2017 with the vision of “building a circular supply chain to power a sustainable world.” Batteries are comprised of a cathode (containing lithium, nickel, cobalt, and manganese), an anode (containing graphite), a separator/electrolyte, and copper foil to allow electrons to travel through the battery. The company currently produces cathode materials at its facility in Nevada and is beginning production of copper foil there as well. This copper foil, primarily used in the anode, is currently manufactured overseas in Asia, with no US production. The loan will be received in tranches based on construction and production progressing at Redwood’s recycling facilities in Nevada as well as a recently announced campus in Charleston, South Carolina. Panasonic is the first customer for Redwood’s cathode and anode materials for their jointly-owned with Tesla Nevada factory and Kansas facility set to open in 2025.

Gold

Gold giant Newmont bids $16.9B for Newcrest

US-based largest gold miner in the world Newmont has submitted a bid worth $16.9B to buy Australian rival Newcrest. The combined company would be nearly twice as large (by market cap) as next largest gold producer Barrick, and would place four of Australia’s five largest gold mines under one company’s control. Newcrest was initially founded as Newmont’s Australian arm, but was spun out in 1990. Newcrest, whose stock is still a third below its 2019 all time high, is considered cheap by some due to the longevity of their gold assets, so it is possible Newmont increases their bid. The announcement follows the 2018 Randgold acquisition by Barrick and 2022 Yamana Gold acquisition by Agnico and Pan American, representing continued M&A activity in the gold sector.

Key Takeaways

Lithium discoveries continue to be made around the world, but won’t contribute to supply chains for a decade plus.

Increased copper output will come from existing projects, largely in Africa.

Auto manufacturers continue to invest in raw materials, as in GM with Lithium Americas and Vale base metals, or Redwood partnering with Panasonic.

That’s all for this week. Thank you for reading, and if you have not yet, please consider subscribing.

- Teddy