This Week in Critical Minerals - #3

Lithium mining in North America, copper a critical mineral, and battery startups

Welcome to the third issue of This Week in Critical Minerals, where I cover the mining and resource processing projects and technologies being built around the world.

Thank you for joining me! Let’s dig into it.

Lithium

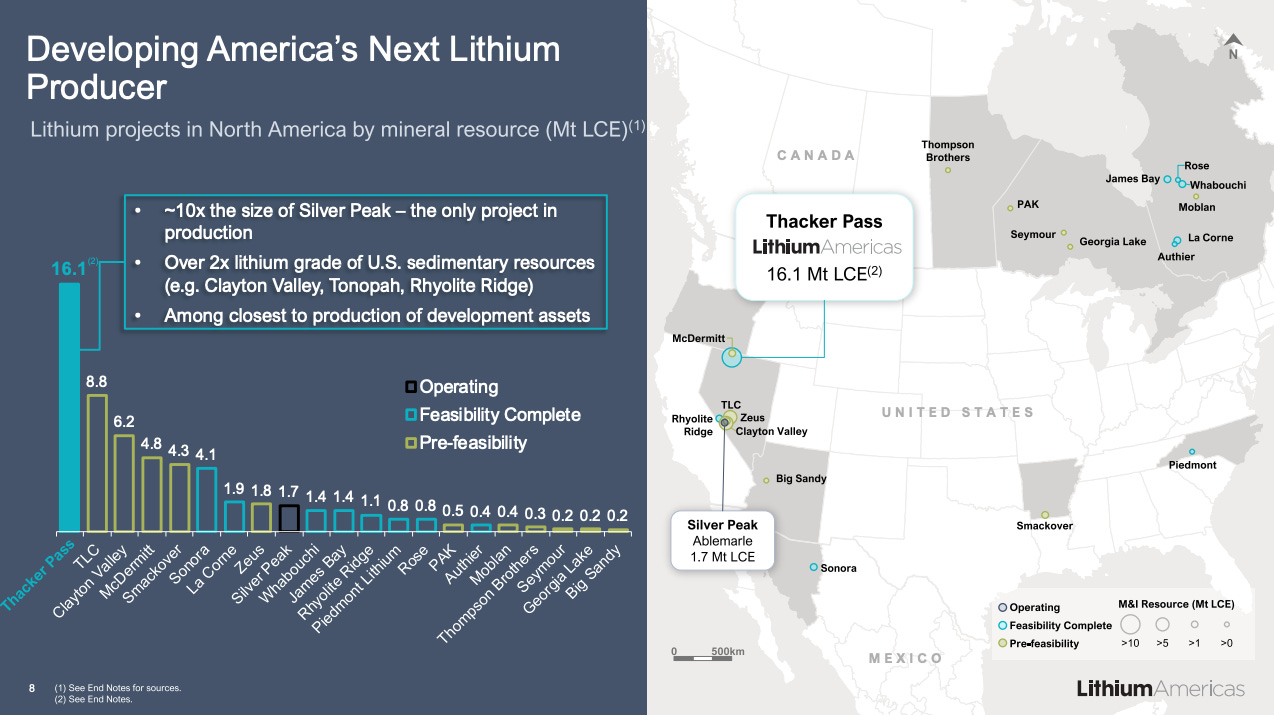

GM invests $650MM in Lithium Americas

This week General Motors announced a $650MM equity investment in Lithium Americas to develop the Thacker Pass lithium mine in Nevada. The US Bureau of Land Management approved the mine for construction in January 2021, but progress quickly stalled as Lithium Americas was faced with lawsuits from several parties. This includes lawsuits from Indigenous peoples concerned with the mine’s impact on ancestral lands, a rancher concerned with the project’s water use, and environmental groups claiming the project threatens several endangered species. The US District Court of the District of Nevada is expected to rule in the next few months on whether an error was made in the mine’s initial approval, or if construction at Thacker Pass can continue. GM’s investment will be made in two tranches, with the first tranche of $320MM for 10% of the company contingent on a favorable ruling in the District Court’s impending ruling. The second part of the investment is expected to be made late this year after Lithium Americas splits into two companies, one holding the American assets (including Thacker Pass) and the other containing the company’s Argentinian assets. GM’s further investment would be made in the American entity. Production at Thacker Pass is expected in the second half of 2026, with GM receiving all lithium carbonate produced by the company is the first phase of the mine.

GM’s investment is a vote of confidence in Lithium Americas and a domestic lithium supply chain. With a precarious ruling deciding the fate of what could be the third largest lithium project in the world, GM has backed what could be a very important company in the transition to electric vehicles.

Sayona Mining completes trial at crushing plant

Canadian company Sayona Mining successfully completed a trial of the crushing stage at its North American Lithium (NAL) concentrator plant in Quebec. The plant will convert spodumene ore into spodumene concentrate (a lithium chemical required to make lithium carbonate which is used in batteries). NAL was bought out of bankruptcy in 2021 by Sayona Quebec, a joint venture 75% owned by Sayona Mining and 25% owned by Piedmont Lithium (who in turn own 19% of Sayona Mining). Prior owners had invested ~$400MM in developing the NAL mine and concentrator plant; Sayona is restarting these operations with the existing infrastructure. Piedmont Lithium has an offtake agreement with NAL to supply Piedmont with spodumene concentrate for its lithium carbonate plants being built in North Carolina and Tennessee. Mining is also expected to resume on-site, as well as at other Sayona-owned projects in Quebec. There are also plans to construct a lithium carbonate processing plant in Quebec, which would over the long term be supplied with NAL spodumene concentrate, as the offtake to Piedmont Lithium is phased out.

When commissioned later this quarter, the North American Lithium project will be one of only a few producing lithium assets in North America, representing a critical part of a Canadian and American lithium supply chain.

Copper

Pebble Mine blocked by EPA

The Environmental Protection Agency, citing the Clean Water Act of 1972, has vetoed Pebble Mine, a proposed gold, molybdenum, and copper project owned by Northern Dynasty Minerals over concerns in the storage of mining waste. The mine would require the construction of a massive dam and tailings (mine waste) storage pond, which could risk contaminating groundwater and the surrounding aquatic ecosystem, particularly in this seismically active area. The region of Alaska Pebble Mine is situated in, Bristol Bay, is home to the world’s largest sockeye salmon fisheries and is an ecologically sensitive watershed. Bristol Bay’s salmon industry generates roughly $2.2B in economic activity yearly and supplies half the world’s sockeye salmon. The EPA’s action will also block future mining in the area, in an effort to protect the environment and Alaska’s fishing industry. Pebble LP CEO John Shively said that the EPA’s move is “not supported legally, technically, or environmentally,” and it looks like Pebble will challenge this decision in court. The project has been controversial for nearly two decades, with formers presidents Obama and Trump against the proposed mine. This is the second week in a row where a major mining project has been blocked in the US, following the decision on Twin Metals last week.

Pebble Mine is emblematic of the conflict between environmental protection and mineral resource development. Though the US is in drastic need of a domestic critical mineral supply chain, it seems clear that projects as controversial as Pebble will not get built.

MMG shuts down Las Bambas mine in Peru

Chinese mining giant MMG (Minerals and Metals Group) has placed the Las Bambas copper mine on care and maintenance, halting production at one of the largest copper sources in the world which at full production accounts for 2% of global copper output. MMG has cited community unrest related to the ongoing protests in Peru (as I wrote about last week) as reasoning for this temporary shut down. Protests which have been ongoing for about 8 weeks and cost 58 lives have put 30% of Peru’s copper output at risk, a significant portion from the world’s second largest producer.

Decreased production has been bolstered slightly by the rapid ramp up of mining giant Anglo American’s Quellaveco copper mine in the south of Peru. Quellaveco has thus far not been significantly impacted by political instability in the region, but that could change. Quellaveco’s development has led Anglo American to report a 3% rise in copper production in 2022, compared to decreases in other copper majors like Glencore and Antofagasta.

Copper finds allies in US Senate

Kyrsten Sinema, Independent Senator from Arizona, sent a letter to Secretary of the Interior Deb Haaland urging her to reclassify copper as a critical mineral. Sinema recruited Senate colleagues from both sides of the aisle in backing this letter, including Mark Kelly (D-AZ), Joe Manchin (D-WV), Mike Braun (R-IN), Raphael Warnock (D-GA), and Mitt Romney (R-UT). As part of the Mineral Security provisions of the Energy Act of 2020, the US Geological Survey evaluates all elements/minerals and compiles a list of “critical minerals” based on supply chain risk. The USGS will reassess the critical minerals list every 3 years, but they are able to add to the list before then if conditions change that may affect a mineral’s designation. The initial critical minerals list was compiled using 2018 production data, but since then the share of US copper consumption met by imports has grown from 33% in 2018 to 41% in 2022. Designation as a critical mineral would allow the federal government to better allocate capital and resources to domestic copper projects (including mining, processing, and recycling), strengthening the United States’ copper supply chain, as seen with lithium projects due to investment from the recent Inflation Reduction Act.

Batteries

Australian battery group close to acquiring Britishvolt assets

Recharge Industries, an Australian battery group, has been selected to buy what remains of Britishvolt, failed British battery startup that had plans to build a £3.8B battery factory in Northumberland. Britishvolt entered administration just a few weeks ago. Recharge owns a variety of battery technologies, and the company plans on building a battery startup in Geelong, Australia. While the company Britishvolt is over, there is still a possibility of a battery facility due to covenants allowing a factory at the site. It is also possible Recharge chooses to commercialize Britishvolt’s prototype battery technology.

Our Next Energy lands $300MM Series B

Battery startup Our Next Energy (ONE) closed a $300MM Series B financing round at a $1.2B valuation led by Fifth Wall and Franklin Templeton. This come just 16 months after the $25MM Series A and 11 months after the $65MM Series A1 last March. ONE aims to be the first US producer of lithium iron phosphate (LFP) battery cells at its planned factory in Michigan. The LFP battery chemistry, while invented in the US, is produced almost entirely in China, notably by Chinese producer CATL. LFP is a lower cost battery cell chemistry than conventional nickel cobalt manganese (NCM) chemistries used in most American electric vehicles. While cheaper, EVs made with LFP cells tend to have lower range than conventional alternatives. ONE received $220MM in subsidies/incentives from the state of Michigan and aims to be producing at 2 gigawatt-hours of capacity by the end of next year. Battery investment in the US is thriving with both federal and private market support, and ONE shows the importance of a diversity of battery cell types being produced in the US.

Key Takeaways

Lithium production in North America is on the rise. GM’s backing is a major breakthrough for Lithium Americas and North American Lithium’s restart is imminent.

The Pebble Mine decision demonstrates that environmental protection remains of utmost importance to the current administration.

There is momentum for copper’s designation on the critical minerals list which could lead to increased US investment in the metal.

LFP battery production is coming to Michigan with ONE’s latest fundraising.

That’s all for this week. Thank you for reading, and if you have not yet, please consider subscribing.

- Teddy