This Week in Critical Minerals – #21

Mining policy, copper, rare earths, lithium, and uranium news

Welcome back to It’s Time to Mine.

Policy

China bans exports of gallium, germanium, and antimony to the US in response to chip sanctions. The intense sequel to China’s 2023 export ban has arrived: earlier this week, the Chinese government announced an export ban on gallium, germanium, antimony, and superhard minerals. Back in the summer of 2023, China had curbed the export of eight gallium and six germanium products, and the following winter, the country restricted the export of technology to make rare earth magnets, so this is far from unprecedented. However, this iteration is much more sweeping and comes on the heels of the Biden administration’s restrictions on the sale of American and foreign high-bandwidth memory chips necessary for AI applications to China, clearly showing this is a retaliatory action before a pro-tariff Trump administration. How can the U.S. handle this? Start aggressively exploring for, mining, and refining more critical minerals domestically. We can push diplomacy or nudge allies to produce more (China has been especially sharp with investment in Africa), but there’s plenty of room for the incoming Trump administration to jumpstart domestic exploration and production to lessen the blow of a metals trade war.

Copper

Top copper miner Chile gets back to pre-pandemic output levels. With ore grades declining, major miners are spending billions to open new mines, increase mine throughput, and improve copper recovery from existing operations. Chile’s state-owned miner Codelco reported that the company exceeded its own monthly production goal in October, and overall mines in Chile have been as productive as they were in 2019. While copper and the incredible Chilean economic growth are intertwined, production in the last couple of years has been lackluster. As we see more political and economic attention diverted to the energy transition, Chile is strategically positioning itself to capitalize on increased demand for the red metal.

Rare Earths

Madagascar lifts its 2019 suspension on Energy Fuels’ Toliara critical minerals project. The Colorado-based firm is well-known for its uranium production, operating the only conventional uranium mill in the US (White Mesa in Utah) and several small mines. Though uranium is a large and critical market, management wanted to diversify towards the also growing markets for titanium, zirconium minerals, and rare earth elements. As a result of this, Energy Fuels acquired the Toliara project through its purchase of Australian mineral sands developer Base Resources in April 2024. Resource-rich developing countries battle the dilemma of being too strict on foreign extraction which limits government revenue while trying to avoid the resource curse, so hopefully, this move signals a step toward collaboration that attracts investment while safeguarding long-term economic stability.

Lithium

Lithium Argentina is seeking to redomicile in Switzerland. Ask someone, “Where do you want to domicile your company?” and Switzerland will probably be among the options. Lithium Argentina, following the earlier move of Solaris Resources, has opted to domicile the company in Switzerland, specifically Zug. You don’t need to be watching the mining industry to know the absurd amount of companies registered in the low-tax canton - 38,547 at the end of 2022. In mining, Zug is almost synonymous with mining and metals trading giant Glencore. However, this move is not totally unexpected even ignoring the obvious tax benefits. This move follows Solaris Resources’ departure from Canada this year following a national security review of Zijin Mining’s C$130M in its Warintza project in Ecuador. Lithium Argentina’s main project Cauchari-Olaroz is a joint venture with Chinese company Ganfeng (44.8%/46.7% split respectively). Though western opposition to Chinese investment and partnerships is increasing, the capital and technical expertise that the Chinese bring is something most partners cannot match. The question now for miners may be: is it worth the move to accept Chinese capital?

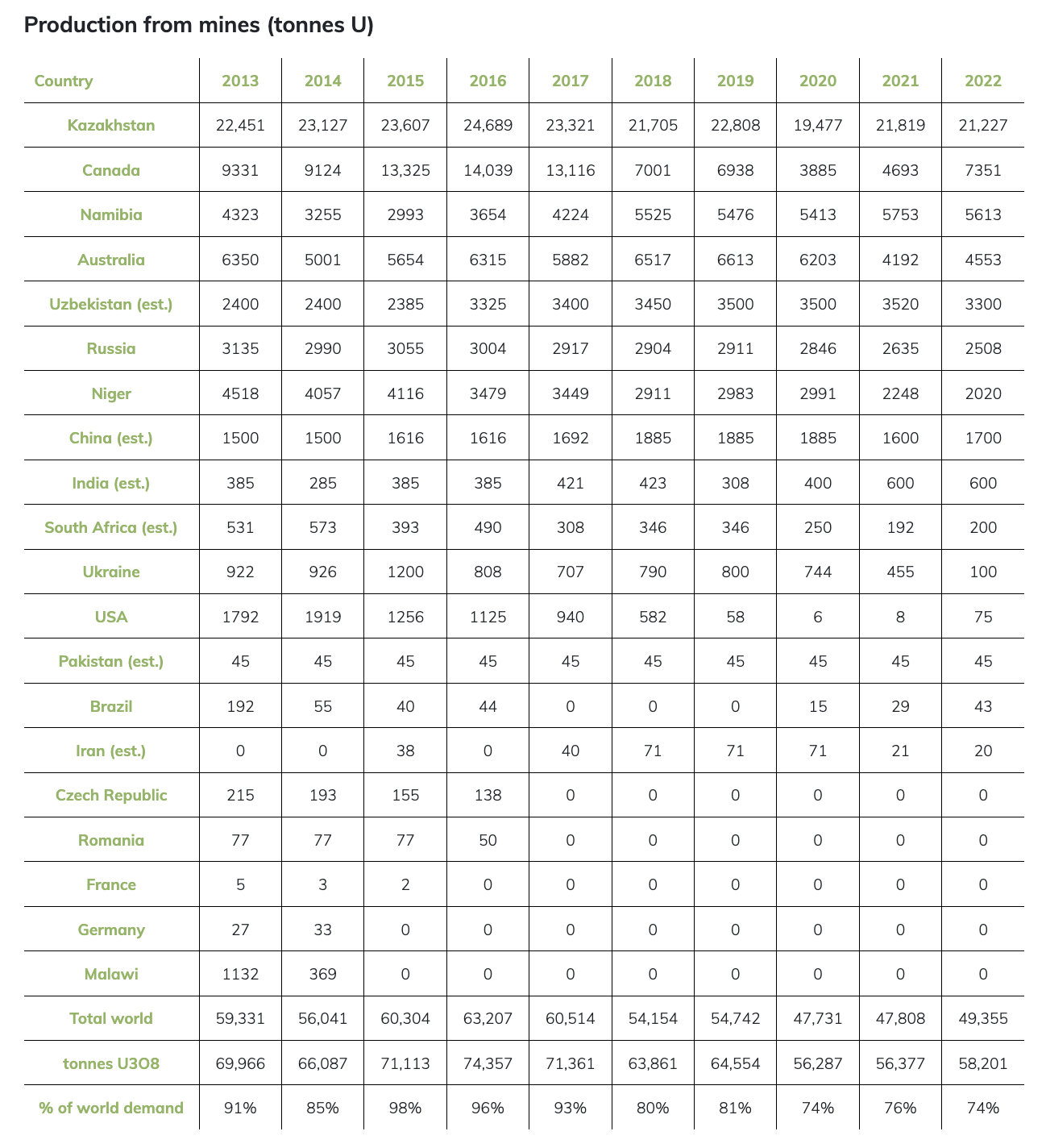

Uranium

Possible tariffs worry Canada uranium miners as they boost output to meet US demand. President-elect Donald Trump’s proposed 25% tariffs on all Canadian and Mexican goods has rattled many in the commodities world. Canada is a vital source of metals and critical minerals, including uranium where the country is the second largest producer, with 85% of production being exported. With Russia banning the export of uranium to the US earlier this year, Canadian companies like Cameco are pushing to increase production to fill the supply gap. Though tariffs can be a tool to incentivize domestic manufacturing or sourcing of raw materials, mines take time to come online. Canada is a critical ally and supplier to the US, thus Canadian uranium producers like Cameco are in a better position than most others to negotiate against tariff proposals and capitalize on a strong push by Western nations to source from allies.

Other Mining News

Northern Star Resources to buy De Grey Mining in $3.3 billion (A$5 billion) deal. Northern Star is the largest gold miner in Australia with 1.65-1.8 Moz expected production in FY2025. Their all-share deal with one of Western Australia’s most exciting gold explorers represents a 36.8% premium on De Grey’s Friday share close of $0.99 (A$1.52). The jewel in the crown is De Grey’s Hemi project which is expected to produce over 500,000 ounces of gold over its first five years. Consolidation has been a big theme in mining over the past few years, especially among the majors like Rio Tinto and BHP, but seeing blockbuster deals like this (which could be one of the largest price tags for a gold project in recent memory) shows the continued bullish sentiment of the gold market.

| A guest post by

|

What are the chances new mines in the US are going to start opening with this new administration?

Great post - I'm really hoping the china decision will re-ignite the US mining industry in a way we've never seen.